The Return of Mercantilism

Reaganomics is dead, free trade has faltered, and the rise of neo-mercantilism demands bold new ideas to shape a better global future.

By Harral Burris

"The crisis was not a failure of the free market system," declared President George W. Bush in November 2008, "…and the answer is not to try to reinvent that system. It is to fix the problems we face, make the reforms we need, and move forward with the free-market principles that have delivered prosperity and hope to peoples across the world."

Unfortunately, Bush was wrong. I cannot imagine today's politicians, Democrat or Republican, voicing the same opinion. Trump's second election proved the final repudiation of free market ideas. The 2008 financial crisis broke the system and an economic era that began with Reaganomics ended in global bankruptcy. Only an international financial system willing to print and pump money, especially dollars, into the worldwide economy kept it from falling into a depression. What could have been a plane crash has turned into an awful, sickening, slow-motion train wreck. The threats to democracy around the globe are part of that ongoing disaster.

The end of an economic era is a significant event. Since the early modern world, there have been three prominent economic philosophies: mercantilism (exploitation of colonial resources for the wealth of imperial masters), market capitalism (free trade to profit investors), and social welfare capitalism (balancing government and business power for the common good.)

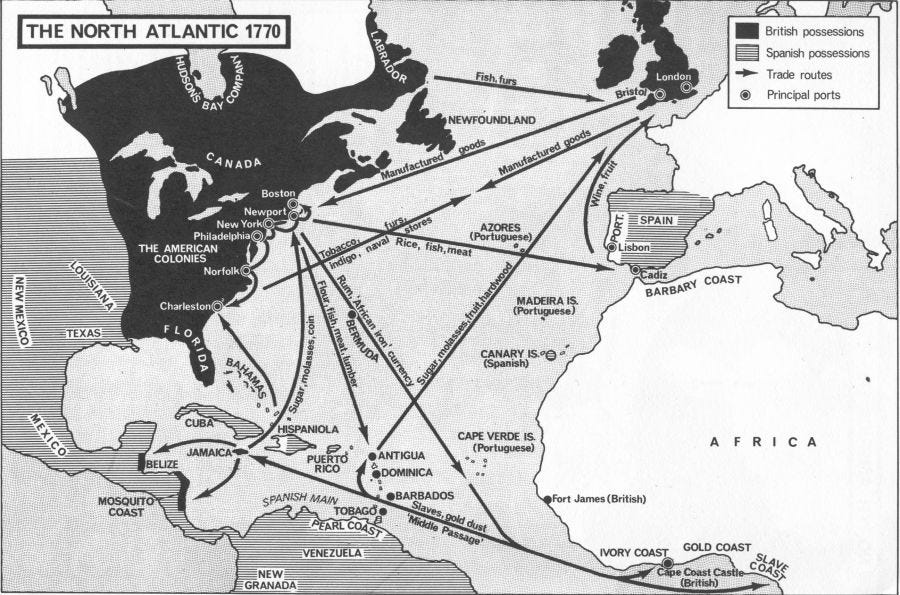

Mercantilism dominated the Age of Discovery, beginning in the sixteenth century. European powers – Portugal, Spain, the Netherlands, France, and England – sent their agents across oceans to find resources, from coffee to cotton, that they could plunder for their capitals. European factories turned those products into manufactured goods which they re-sold to domestic consumers and their colonies in return for currency, including gold and silver. Mercantilism enriched the metropole as it impoverished poor citizens and colonial subjects.

In 1846 Britain repealed its so-called "Corn Laws," opening the empire to free trade in agricultural goods. Reform leaders recognized that more open trade in foodstuffs would increase availability and lower costs for the island kingdom, which depended on imports. London abandoned mercantilism for free trade capitalism.

This is when the influence of radical thinkers like Adam Smith was at its height. Free trade meant finding the least expensive setting to produce goods, not relying on manufacturing or agriculture in the metropole over the colony. Instead, the emphasis was on circulating goods as efficiently as possible, trading them among countries for the widest distribution. Businessmen in the City of London, Amsterdam, and other growing trading ports profited from managing this wider trade through their investments. Unlike the mercantilist empires dominated by monarchs, capitalist governments empowered merchants, bankers, and, of course, lawyers.

This era of no-holds-barred, bare-knuckle capitalism produced tremendous wealth, the corruption of the Gilded Age, and the massive income inequality that followed. The 1929 stock market crash and the ensuing depression effectively ended capitalism as the world knew it. But old orders fall quickly and abruptly, and replacements take longer to form. It is no coincidence that the decade of the 1930s, an interregnum between different modes of capitalism, was also the decade of fascist autarchy and Soviet communism – two systems that promised to use state force to make capitalism more beneficial to loyal citizens.

Frightened by the threats of fascism and communism, capitalist leaders looked to tame their system, focusing on social welfare as well as profits. For programs like the New Deal in the United States, that meant increased cooperation between government and businesses to ensure wider access to jobs, housing, food, and safety for citizens. Government grew to regulate markets for the interests of the public, while still allowing profits for investors. Social welfare capitalism always had its opponents, but it supported a period of remarkable prosperity and stability for wealthy nations after the Second World War.

In the late 1960s, President Lyndon Johnson tried to fight the Vietnam War and expand social welfare through his Great Society program. These combined efforts were too much, especially without significant tax increases, which he opposed, to fund government expenses. An inflationary spiral resulted, and by the next decade, US gold reserves reached a historic low. The United States became a net importer of goods and capital, economic growth slowed, and joblessness became a major problem in formerly industrial (now "rust belt") areas.

Jimmy Carter's unhappy presidency, recently recounted at his funeral, was a result of this crisis in social welfare capitalism. Two emerging political figures, Margaret Thatcher in Great Britain and Ronald Reagan in the United States, pronounced this system dead, even as they continued to rely on many of its programs – including Social Security and Medicare.

"Reaganomics" called for much less government intervention in the private parts of the economy. Restrictive regulations and tax rates diminished, and the world entered a new era of global growth. Trade barriers fell and national economies became more interconnected than at any time since before the two world wars. As supply chains stretched further, capital flowed rapidly from domestic to international investments. "Globalization" made the rise of a digital economy possible around hubs of talent, investment, and entrepreneurship.

But all things must pass, and the growth of the 1980s and 1990s led to the real estate and financial excesses of the early twenty-first century. The Reagan-inspired economic system collapsed in 2008, but like the period between the Great Depression and the Second World War, a new financial order has taken some time to coalesce. Although massive government spending, which still continues, avoided economic collapse in 2008, the global economy never fully recovered. While the very rich became more prosperous in this low-interest, low-growth environment, few others benefited. Many citizens found themselves working harder than ever just to keep up. Income disparities reached levels not seen since the 1930s.

With the election of Donald Trump in 2016, the Republican party lurched to the right and embraced protectionism with tariffs against competitors and allies alike. Millions of American voters associated free trade with lost jobs and dependence on precarious supply chains for essential products. Pandemic shortages left traumatic scars. President Biden reversed some of the Trump tariffs against allies but tightened trade restrictions against China and sanctions against Russia and Iran. The country did not return to long-standing free trade policies.

This new era resembles a form of mercantilism, modified for the 21st century. The globalization of trade, a key element of all post-mercantilist economies, is now running in reverse. Not only are tariff barriers going up worldwide, but democracy itself seems to be in decline, with nations turning to authoritarian states to control trade for the benefit of government-favored domestic interests.

Neo-Mercantilism promises more concentrated wealth, trading blocs, and intrusive political leaders (often backed by super-wealthy supporters.) In the current economic environment, the idea that the free market system demonstrably failed enables a return to autarchic government policies. History offers little reason to believe this shift will benefit any society. The challenge for the coming years will be to design a better alternative.

We cannot go back to failed free-trade capitalism, but a return to mercantilism promises even worse conditions. The time for creative thinking about a new system is upon us. The dying past can motivate a more hopeful future if we are willing to think and act in new ways. Now is the time for big thinkers and new ideas.

Hal is a retired investment professional with 40 years of experience in money management. The interface between geopolitics and global investments has always been his area of specialization. History has always been one of his interests and passions, in fact, that’s how Hal and Jeremi became friends in Madison, Wisconsin.

Paul Krugman, on his substack, has engaged this frequently, China with a plus trillion dollars trade imbalance and the rest of EU nations with under water imbalances, and, the USA with a thriving economy, for the moment, Trump can easily return us to Oct, 1929